The real question isn’t whether Visa and Mastercard are leading the Digital ID agenda — it’s whether they, alongside the central banks, can actually pull it off without rolling out central bank digital currencies (CBDCs). On the surface, a “Digital ID” sounds harmless, even practical. But behind the glossy marketing lies something much deeper: a system built to merge personal data and biometrics while quietly stripping away privacy. Once fully integrated, it determines how you spend your money, what services you can access, and ultimately, who controls your assets.

This isn’t limited to finances. It stretches into every corner of life — education, healthcare, food supply, farming, transport, property ownership, and even technology. All of it tied together through one Digital ID, linked to your bank, and monitored through a social credit-style framework.

This isn’t theory or speculation. It’s all outlined in the documents and plans published by the Bank for International Settlements (BIS), central banks, the World Bank, major financial institutions, and payment giants like Visa and Mastercard — with full government cooperation.

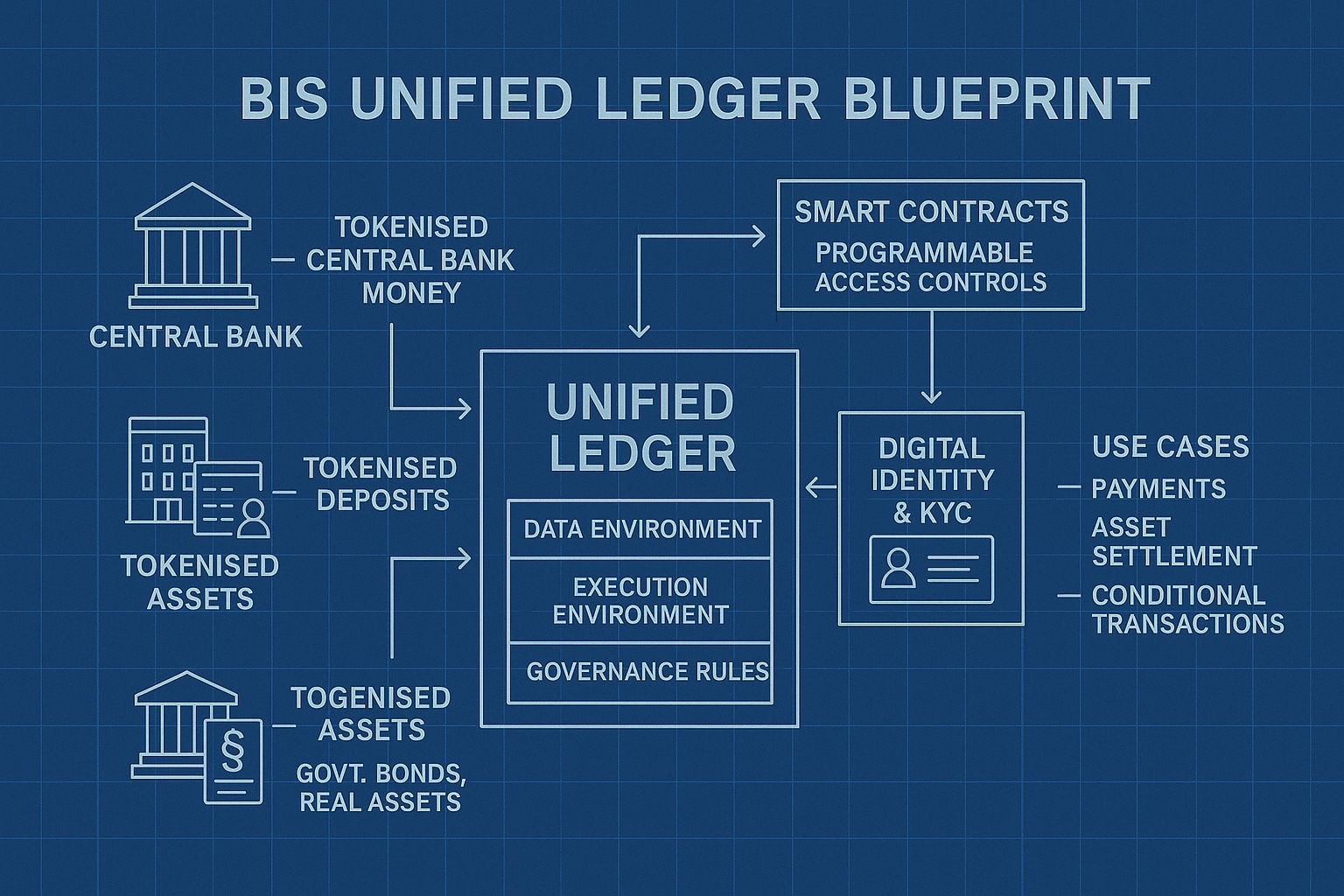

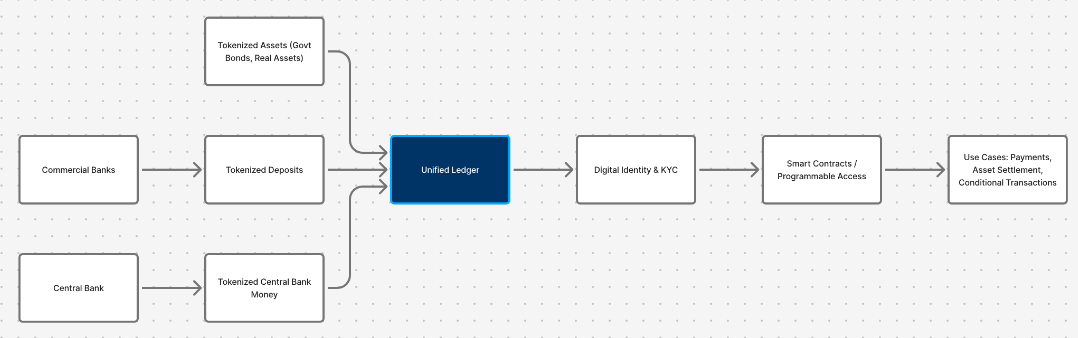

To put it simply, the BIS envisions a world where everything you own — your money, your house, your car — is turned into a digital “token” inside a single, unified global ledger. Each token could be governed by “smart contracts” — programmable rules dictating how, when, and where your assets can be used. It’s not just about convenience. It’s about control.

By using fear of cyber attacks on any single institution, big Gov and financial institutions want everyone to believe that consolidating all data and assets of a person’s life into tokens under a Digital ID will somehow protect them from attacks by having everything in one location.

Though many are under the impression that the battle is against the ushering in of CBDCs, it would seem that all of the appropriate financial rails and interoperability are already in place, or darn close to it, to expand on the mountain of identity verification processes already dialed in, to initiate the all-in-one Digital Identity and lock those dominoes into place.

This digital world they intend to manifest is being fashioned to look like a convenient and necessary way everyone must live, and as they build these “rails” of prison cells, consumers are sinking further into debt and relying more and more on credit cards.

The Federal Reserve Bank of New York issued a report noting that credit card balances in Q4 of 2024 increased by $45 billion to a record high of $1.21 trillion, while also reporting elevated delinquencies. Total household debt also rose by $93 billion, reaching $18.04 trillion in the fourth quarter of 2024.

Visa and Mastercard are at the forefront of this takeover and if they succeed, the monitoring, tracking, and control will be immeasurable and there will be no going back. Consumers need to think twice before using credit cards and use cash as often as possible, while state legislators need to get on board with implementing creative legislation with independent systems that not only provide protection for the citizens of their state, but build strong financial freedom with the ability to operate utilizing cash, precious metals, and unique structures as pointed out in this article.

“I get why China would be interested. Why would the American people be for that?” – Neel Kashkari, President of the Minneapolis Federal Reserve, ‘The Threat of Financial Transaction Control,’ the Solari Report, February 24, 2024.

Brief History of Visa & Mastercard

Visa

The first major credit cards emerged from the 50s to mid-60s. Bank of America issued the first consumer credit card with revolving credit in California in 1958, expanding their network through licensing agreements with banks throughout the nation by 1966. The network spread out internationally by 1974, prompting a rebranding in 1976 of the BankAmericard to Visa, an internationally recognized term that conveys universal acceptance.

By 2007, several regional Visa businesses from around the globe merged to form Visa Inc., and the following year, on March 18, 2008, the corporation went public. Visa’s initial public offering (IPO) sold 406 million shares at $44 per share totaling $17.9 billion, one of the largest in U.S. history. Then on March 20, 2008, the underwriters of the IPO, which included JPMorgan, Goldman Sachs, Bank of America, Citi, HSBC, Merrill Lynch, UBS Investment Bank and Wachovia Securities, exercised their over-allotment option by purchasing an added 40.6 million shares, raising the overall IPO shares to 446.6 million for a total of $19.1 billion.

Their Board of Directors includes current and former CEOs, CFOs, and COOs of Carney Global Ventures, Rite Aid Corporation, PepsiCo, Gap, Stanley Black & Decker, Visa, and The Clorox Company.

Over the decades, Visa has faced a myriad of legal actions and disputes concerning anticompetitive practices and high fees. As recently as 2019, a settlement of $5.5 billion was reached in a class-action lawsuit by merchants alleging that Visa and Mastercard engaged in price-fixing practices with regards to swipe fees charged to merchants and the credit card networks unfairly interfered when merchants encouraged less expensive forms of payment such as cash or checks. Additionally, the Department of Justice launched an antitrust probe against Visa in March of 2021. The investigation has remained ongoing according to Visa’s SEC filing in mid-2023.

These cases aren’t just isolated disputes — they reveal a consistent pattern: consolidation of financial power and resistance to any challenge that threatens that dominance. For decades, Visa has operated not merely as a payment processor but as a gatekeeper, dictating who gets to move money, how it moves, and under what conditions. And now, as the conversation shifts toward Digital IDs and programmable money, Visa stands at the center once again — the same network that built the rails for global commerce may soon become the rails for global control.

Mastercard

Competitors to Visa arose in 1966 to form the Interbank Card Association (ICA), which later became Mastercard International. The original bank members were United California Bank, Wells Fargo, Crocker National Bank and Bank of California. The group introduced the Master Charge card which ultimately became known as Mastercard in 1979.

The ICA expanded their network globally, merging with Europay International in 2002 and then converting from a membership association into a private share corporation in preparation for their initial public offering that commenced in 2006. The IPO of 61.5 million shares, priced at $39 per share, raised $2.4 billion. Goldman Sachs coordinated a group of four joint book-runners that included Citigroup, HSBC, and JPMorgan. Co-managing underwriters included Bear Stearns, Cowen and Company, Deutsche Bank, Harris Nesbitt, KeyBanc Capital Markets, and Santander Investment.

Their Board of Directors is made up of current and former CEOs as well as other high level positions from US Bancorp, The Carlyle Group, Mastercard, Verizon, Goldman Sachs, and BeyondNetZero.

Similar to Visa, Mastercard has been plagued by a number of scandals and legal actions over the years. A 2018 report noted that Mastercard brokered a secret multimillion dollar deal with Google to share credit card data for targeted advertising purposes. Then in 2019, as mentioned above, Mastercard and Visa settled a class-action suit worth $5.5 billion for anticompetitive practices. Furthermore, an SEC filing disclosed that, like Visa, the Department of Justice Antitrust Division initiated an investigation into Mastercard in March of 2023.

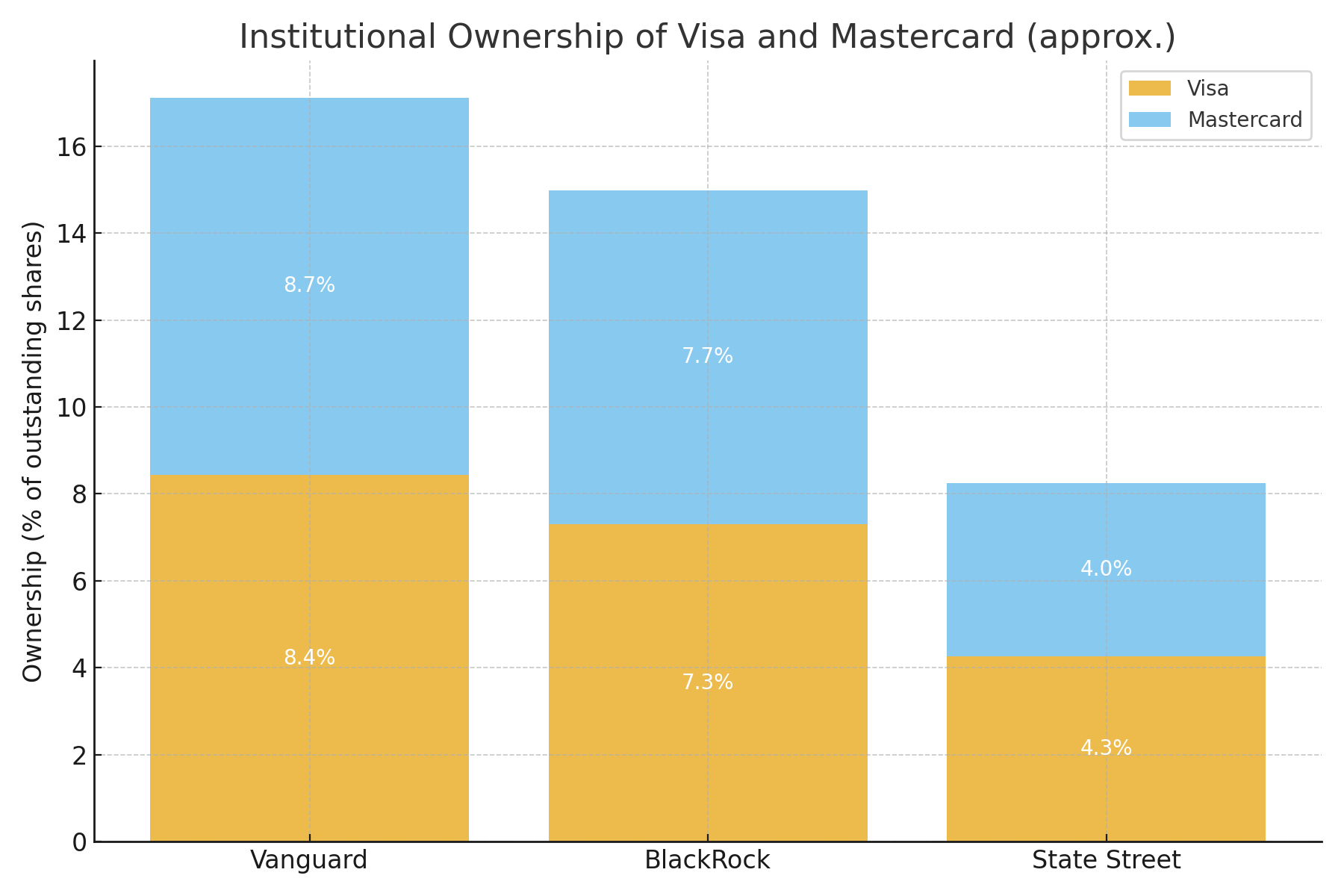

Currently, Vanguard, BlackRock, and State Street are the top three shareholders of both Visa and Mastercard.

Visa & Mastercard Play an Integral Role in Digital IDs & CBDCs

Visa

In 2019, Visa launched B2B Connect, which is a platform that uses blockchain to offer financial institutions a streamlined cross-border payment process. The Visa B2B Connect network is designed to offer digital identity solutions and a “centralized system of record for each and every payment.”

Visa has filed around 44 blockchain-related patents in the United States and roughly 20 additional patent families internationally, many centered around biometric identity tracking, programmable money, and digital asset control systems.

These filings are not about user convenience — they outline the technical foundations for a world where every transaction and identity verification step can be monitored, approved, or denied by design.Examples include:

WO2018222211A1 – “Secure Biometric Authentication Using Electronic Identity”: describes a system that binds an individual’s biometric data — fingerprints, facial recognition, or other identifiers — directly to digital identity profiles on a blockchain, ensuring that every interaction in the financial system is traceable and tied to a verified body.

US20220052852A1 – “Secure Biometric Authentication Using Electronic Identity”: expands the same concept by allowing verification through distributed ledgers, effectively removing anonymity from transactions under the banner of “security.”

US20210353699A1 – “Digital Currency for Interoperable Blockchain Networks”: sketches the infrastructure for linking central-bank digital currencies, stablecoins, and private tokens — a unified web where all forms of money become programmable and centrally observed.

US20220031643A1 – “Digital Asset Tokenization and Settlement System”: outlines how real-world assets — property, savings, even vehicles — could be turned into digital tokens and settled on corporate-controlled blockchain rails, tightening control over ownership and access.

Taken together, these patents reveal a coordinated move toward programmable financial identity, not freedom or privacy. Behind the technical language lies a vision of total visibility and conditional permission — the architecture of a financial surveillance grid disguised as innovation.

In 2020, Visa filed for a patent to create a digital currency using blockchain, which is designed to replace cash. They aim to act as a central entity computer which creates a digital currency by using a serial number and denomination of physical currency. The patent applies to all digital currencies including: Ethereum, CBDCs, pounds, yen, and euros.

Visa also partnered with Ethereum in 2020 to connect its payment network of 60 million merchants to the U.S. Dollar Coin (USDC) developed by Circle Internet Financial.

In September of 2020, the world’s largest cryptocurrency exchange, Binance, introduced a Visa debit card which automatically converted users’ crypto assets into local currency. Since August of 2023, both Visa and Mastercard stepped back from their partnerships with Binance to offer crypto debit cards amid regulatory scrutiny.

In May of 2021, Visa announced the expansion of their Fintech Partner Connect program, matching banks that issue Visa cards with fintech companies that offer digital tools to enable their seamless transition toward “the ultimate goal of accelerating adoption of digital-first innovations” which incorporates digital identity verification. Their fintech partners include: Entrust, Alloy, Global Data Consortium, Idemia, Jumio, Neuro-ID, and Onfido (each outlined in more detail below.)

Visa’s fintech partner, Alloy, is a “global end-to-end identity risk solution” for banks that “enables instant digital identity verification and document verification.”

Global Data Consortium, which was acquired by the London Stock Exchange Group (LSEG) in April of 2022, is another Visa fintech partner. The acquisition by LSEG was specifically designed to “expand its global range of digital identity solutions.” LSEG offers global identity verification supported by biometric and document verification.

Another Visa fintech partner, Idemia, is a “world leader in biometrics” that provides governments with IDway, which is a “suite of digital identity solutions,” that incorporate several components into a unified system. These components, which include civil registries, ID cards, passports, and welfare registries, work together “as a unified system solution to efficiently manage the identities of a country’s population.”

Jumio is yet another Visa fintech partner that claims to be “the leader in online identity verification” and “way ahead of the game in digital identity as well.” Jumio offers solutions to enable their customers to “issue and verify digital identities from trusted sources,” which include smart wallets.

Visa is also partnered with the fintech company, Neuro-ID, a pioneer “in the field of behavioral analytics,” which launched “breakthrough digital identity products” in February of 2022 that incorporate behavioral data.

Onfido, an additional Visa fintech partner, offers a “Real Identity Platform” for digital identity verification powered by AI, which incorporates both biometric and document verifications.

In January of 2022, Visa partnered with the blockchain technology company ConsenSys to offer central banks a platform to test Central Bank Digital Currencies (CBDCs) and Visa products. The platform can enable a system “for central banks to issue and distribute CBDC.”

In December of 2023, Visa partnered with TECH5, an “innovator in the field of biometrics and digital identity management,” to implement a “digital ID-based payment infrastructure and services on a national level.”

On February 19, 2024, Capital One, a major issuer of both Visa and Mastercard, announced it would acquire Discover in an all-stock deal worth $35.3 billion. If this deal goes through it would make it the largest card issuer when measuring outstanding card loans.

Visa is at the forefront of what they call “the token transformation,” offering “diverse tokenization technologies,” to merchants, regional networks, banks and central banks to “build, manage and control their own tokenization capabilities.” The goal to tokenize all assets, information and people into one global unified ledger is one that the Bank for International Settlements (BIS) has been looking at closely, as evidenced by their 2023 report entitled, “Blueprint for the future monetary system: improving the old, enabling the new.” CBDCs would be “core to the functioning” of this tokenized digital space, serving as the reserve currency on the unified ledger.

Mastercard

World Bank President Ajay Banga speaking about the need for governments to create digital identities for their citizens (22 min in), at the 2024 World Bank’s Global Digital Summit on March 5th.

The current president of the World Bank is Ajay Banga, the former CEO of Mastercard. During his tenure at Mastercard, Banga oversaw what the company itself described as a “strategic, technological, and cultural transformation.” Under his leadership, Mastercard expanded its reach into digital identity systems, financial inclusion initiatives, and partnerships with governments and global institutions—the very framework now aligning with the World Bank’s digital ID and “financial inclusion” agenda.

Mastercard markets the safety and convenience features of a range of Digital Identity Services they offer, which includes their digital ID network, for access to “everything from financial and government services, to healthcare, education, travel, shopping,” and more in what they describe as the “digital transformation.” They have published a number of white papers outlining a variety of use cases for their digital identity services on their site.

Mastercard and PayPal have a global strategic partnership, providing several services to PayPal users, while PayPal is one of the frontrunners to move the needle on digital IDs considering they are the largest digital wallet company with 44% of Americans using their services.

In 2016, Mastercard and Visa were both part of the multi-stakeholder workshop for the World Economic Forum’s “A Blueprint for Digital Identity: The Role of Financial Institutions in Building The Digital Identity.” On page 41 they describe “identity” as “a collection of pieces of information that describe an entity” such as “age, height, date of birth, fingerprints, health records, preferences and behaviors, telephone metadata, national identifier number, telephone number, email addresses, and assets,” for starters. On page 95 they explain how new capabilities for financial institutions would include: digital identity attributes tied to payment tokens, digital tax filing, and tracking total asset rehypothecation. Mastercard and Visa are both “strategic partners” of the WEF.

In 2018, Mastercard served as one of twenty experts on the UN’s “high-level panel on digital cooperation,’ co-chaired by Melinda Gates and Jack Ma, which produced the report titled “The Age of Digital Interdependence.” The report states that “The immense power and value of data in the modern economy can and must be harnessed to meet the SDGs” (UN sustainable development goals). On page 10 of the report it states “McKinsey & Company studied seven large countries and concluded that digital ID systems could add between 3 and 13% to their gross domestic product.”

In December, 2018, Mastercard partnered with Gavi with the purpose of “efficiently delivering vaccines to millions of children, tracking identity and immunisation records in a digitised manner and incentivising the delivery of vaccines,” by deploying the Mastercard Wellness Pass chip card to those in various countries. It utilizes tokenized biometrics to “adhere to vaccination cycles.”

In March of 2019, Mastercard introduced their new framework for the evolution of digital identities, with their platform operating at the center. Mastercard’s framework envisions their role as a central coordinator bringing together “stakeholders” including banks, governments, and individuals to issue and verify digital identities as a condition for accessing goods and services. In their report, Mastercard says, “we are uniquely positioned as a user champion for digital identity,” considering their “experience in governance and operating networks,” as well as their focus on financial inclusion, data privacy, and investments in a “global infrastructure.” Mastercard says they “will facilitate the service platform and network,” which incorporates “core technologies” such as blockchain and biometrics.

Mastercard representatives contributed to the World Economic Forum’s January 2020 report entitled “Reimagining Digital Identity: A Strategic Imperative,” in which digital identities are central for access to healthcare, financial services, food, travel, humanitarian aid, online activity, government services, phone services, and smart cities.

In September of 2020, Mastercard announced the launch of their CBDCs testing platform for central banks to simulate the “issuance, distribution and exchange of CBDCs between banks, financial service providers and consumers.”

Mastercard collaborated with the Good Health Pass initiative to “develop a blueprint for organizations to adopt and implement” digital health credentials, otherwise known as Covid passports, in 2021.

In April of 2021, Mastercard acquired Ekata for $850 million for the purpose of advancing their digital identity efforts “through AI-powered identity verification.” Ekata is described as a “global leader in digital identity verification solutions that provide businesses worldwide the ability to link any digital transaction to the human behind it.”

In June of 2021, Mastercard launched their E-Livestock digital ID for the cattle supply chain. Digital proof of provenance, which is essentially a digital ID for agricultural products and livestock, is becoming more common. The World Bank, which the former CEO of Mastercard now heads, promotes digital identities for farmers to receive financial assistance as well as to increase tracking of the food supply.

Mastercard’s President of Cyber & Intelligence, Ajay Bhalla, has said, “To truly make the digital world work for all, we must rethink traditional notions of digital identity and break down artificial barriers. We need a new model that starts with the commitment to the fundamental individual right – ‘I own my identity and I control my identity data.’ And we need businesses, governments, NGOs, and others to forge partnerships and invest resources in support of a common framework, principles, and standards.”

In April of 2023, Senior VP of Digital Identity at Mastercard, Sarah Clark, outlined Mastercard’s integral role in digital identities globally. She explained that countries are implementing “trust frameworks” to define the roles of digital identity networks like Mastercard’s. The networks then work to become “accredited” under the “trust framework.” Once “accredited,” Mastercard’s network would integrate with “government ecosystems when it comes to digital identities, digital credentials, as they are brought online.” Each country is unique in their “trust framework.” She said, “In the US it’s a state-based approach,” that is “tethered to the existing driver’s license ecosystem,” which Mastercard is looking “to plug into.” Clark added that government-issued digital identities would not be broadly accepted in some countries due to “the fear of government overreaching and tracking everything you do,” which is why Mastercard advocates for “strong public-private partnerships,” such as theirs, to accelerate public acceptance of digital IDs.

In August of 2023, Sarah Clark elaborated on Mastercard’s progress in the digital identity space, stating that they have been “on the leading edge of the paradigm shift that we can all see is happening today with respect to identity.” She noted that Mastercard’s digital ID network is live in two markets – Australia and Brazil. In Australia, legislation, regulations and the Trusted Digital Identity Framework (TDIF) have paved the way for Mastercard’s digital identity network to be implemented. In June of 2022, Mastercard became the first private organization to receive accreditation under the TDIF. She added that Australia is a “template for other parts of the world” and that Mastercard’s digital identity network has “done pilot activities and prepared for launch in two other markets – the UK and the US.”

Would the Digital ID Agenda Even Function Without CBDCs

Keep reading with a 7-day free trial

Subscribe to RevealedEye to keep reading this post and get 7 days of free access to the full post archives.